Blog Details

The United Arab Emirates has transformed into one of the most significant business formers worldwide. It welcomes all entrepreneurs and multinational corporations to its friendly business environment and strategic location. As part of these efforts, the UAE introduces a corporate tax regime policy to promote economic growth without compromising fairness and transparency. As such, it is important for Free Zone persons to learn about the UAE corporate tax regime. This would allow them to follow through the complications of taxation and compliance. This guide aims to provide some of the most comprehensive guides regarding the corporate tax regime of UAE specifically tailored to Free Zone persons, which can help them make informed choices regarding their taxes.

A Free Zone Person refers to a juridical entity that operates within a Free Zone in the United Arab Emirates (UAE).

A Free Zone Person refers to a legal entity that is incorporated, established, or registered within a designated Free Zone in the UAE. This includes companies, branches of foreign entities, and other juridical persons that operate within these specific geographical areas. Under the UAE Corporate Tax Law, a Free Zone Person may qualify for certain tax benefits, including the potential to pay a corporate tax rate of 0% on qualifying income.

A registered branch of a non-resident juridical person located in a Free Zone is classified as a Free Zone Person. In this case, the non-resident parent entity is treated as a Foreign Permanent Establishment. Similarly, a branch of a UAE resident juridical person registered in a Free Zone is also considered a Free Zone Person, while the UAE resident entity is regarded as a Domestic Permanent Establishment under the CT Law.

However, entities that are not juridical persons, such as natural persons or unincorporated partnerships, cannot be recognized as Free Zone Persons.

The UAE Corporate Tax Law provides a unique opportunity for Free Zone Persons to benefit from a 0% Corporate Tax rate on qualifying income. To avail of this benefit, entities must meet specific conditions outlined under the law. A Free Zone Person (FZP) that fulfills all these conditions becomes a Qualifying Free Zone Person (QFZP). Failing to meet even one requirement will disqualify the entity, subjecting it to standard Corporate Tax rates and rules.

Here are the detailed conditions to qualify as a QFZP:

1. Applicability of the Regime to a Free Zone Person:

A Free Zone Person refers to any juridical person that is Incorporated, established, or registered in a Free Zone: This includes branches of non-resident entities and UAE juridical persons registered within the Free Zone.

2. Maintenance of Adequate Substance in the Free Zone

To qualify as a QFZP, the Free Zone Person must demonstrate substantial economic presence by:

3. Compliance with Transfer Pricing Documentation

The Free Zone Person must adhere to globally accepted Transfer Pricing standards, which include:

4. Preparation of Audited Financial Statements

Regardless of revenue levels, the Free Zone Person must prepare and maintain audited financial statements annually to ensure transparency and compliance with regulatory standards.

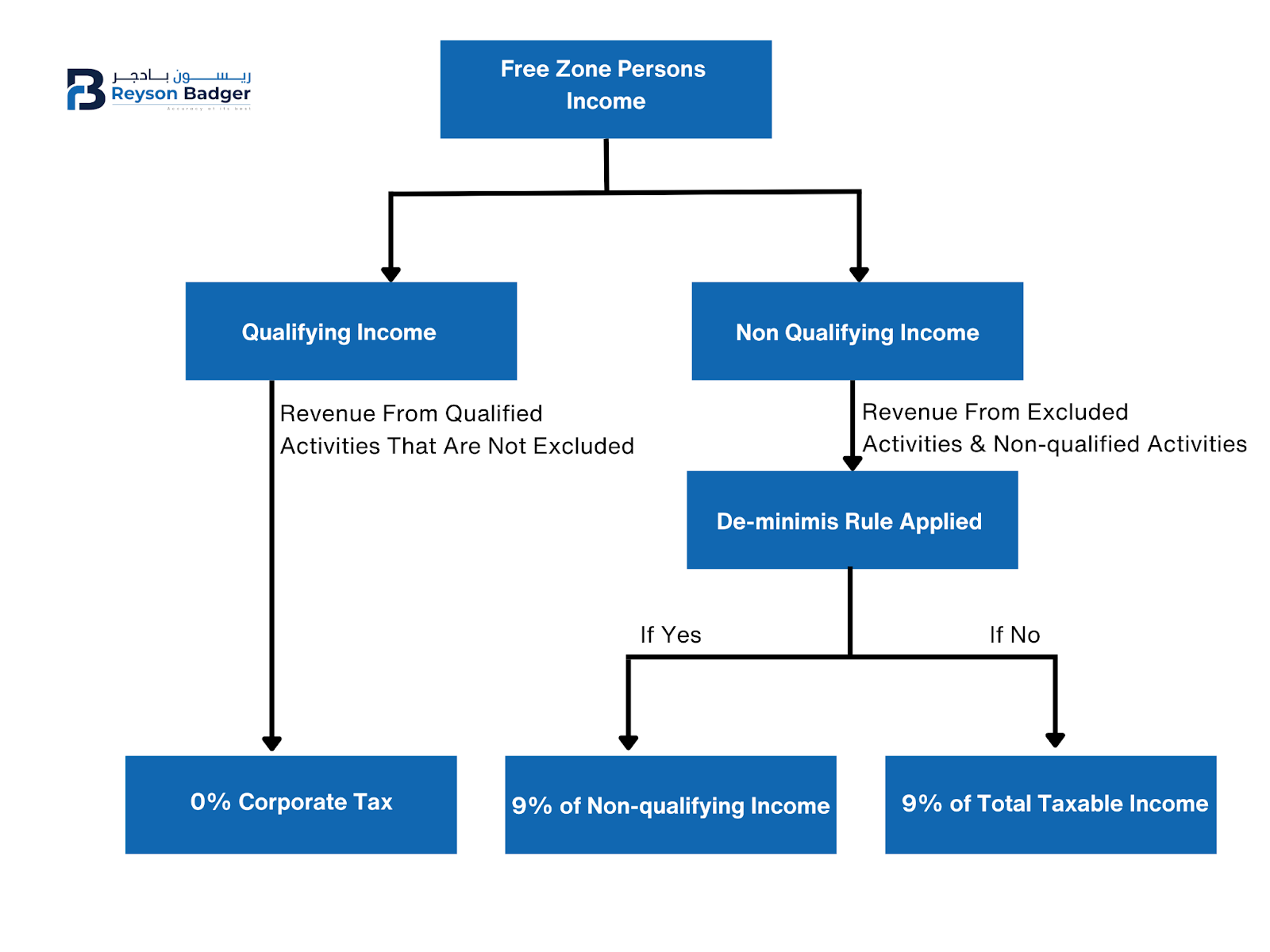

5. Meeting De Minimis Requirements for Non-Qualifying Revenue

The de minimis rule ensures that non-qualifying revenue remains minimal to retain QFZP status:

6. Deriving Qualifying Income

7. Arm's Length Principle Compliance

Meeting these criteria ensures that the Free Zone Person can benefit from the 0% Corporate Tax rate on Qualifying Income while adhering to regulatory and compliance standards.

Qualifying Income refers to income derived by a Qualifying Free Zone Person (QFZP) that is eligible for the 0% Corporate Tax rate in the UAE. This tax advantage supports economic growth and competitiveness within Free Zones. To qualify, the income must arise from specific sources and meet defined criteria, including:

Excluded income, such as that related to domestic or foreign permanent establishments, non-commercial immovable property, and non-qualifying IP, may not benefit from the 0% rate and could be subject to the standard 9% tax.

To maintain this status, a Free Zone Person must also comply with the arm's length principle, maintain Transfer Pricing documentation, and meet other regulatory requirements.

Qualifying activities eligible for a 0% corporate tax rate include the following:

Manufacturing of Goods or Materials

Processing of Goods or Materials

Trading of Qualifying Commodities:

Ownership and Operation of Ships

Reinsurance Services

Distribution of Goods or Materials

Certain activities disqualify Free Zone Persons from the 0% tax rate. These are:

The 0% tax rate applies to Qualifying Income derived by a Qualifying Free Zone Person (QFZP). To qualify, the income must stem from one or more of the following sources:

For income that does not meet the conditions for Qualifying Income, a standard corporate tax rate of 9% is applied. Non-Qualifying Income typically includes:

In practice, QFZPs must ensure meticulous record-keeping and compliance with arm’s length principles, audited financial statements, and other regulatory requirements to benefit from the preferential tax rates.

Step 1: Determine the Taxable Income

Subtract the permitted deductions from the total income to determine the Free Zone individual's taxable income.

Step 2: Apply the Tax Rates

The UAE corporate tax rates are as follows:

Step 3: Calculate the Tax Liability

To calculate the tax liability, multiply the taxable income by the appropriate tax rate.

Step 4: Consider Any Tax Exemptions or Reliefs

Determine if a Free Zone individual qualifies for tax exemptions or reliefs, including a 0% tax rate on qualifying income.

Step 5: Calculate the Final Tax Liability

Take into account any tax exemptions or reliefs and calculate the final tax liability.

Suppose a Free Zone person has a taxable income of AED 500,000.

Taxable income: AED 500,000

Tax rate: 9% (since the taxable income exceeds AED 375,000)

Tax liability: AED 500,000 x 9% = AED 45,000

However, if the Free Zone person is eligible for the 0% tax rate on qualifying income, the tax liability would be:

Taxable income: AED 500,000

Tax rate: 0% (on qualifying income)

Tax liability: AED 0

The UAE offers various tax incentives and benefits to Free Zone persons, making it an attractive destination for businesses. These incentives are designed to promote economic growth, encourage foreign investment, and support the development of industries. Some examples of tax incentives and benefits available to Free Zone persons include:

Understanding corporate tax in the UAE can be a little bit difficult, especially for those in Free Zones. Here are some important things to keep in mind, the tax system is based on where the business is located. Free Zone businesses often enjoy tax exemption. Also, it’s important to register for taxes and file your returns on time.

Because tax laws can be complicated, it's a good idea to get help from experts. At Reyson Badger, we have a team ready to help you navigate these rules and find the best tax strategies for your business. Consulting with our team can help you take advantage of tax benefits and lower your tax liability. This way, you can focus on growing your business without worry.